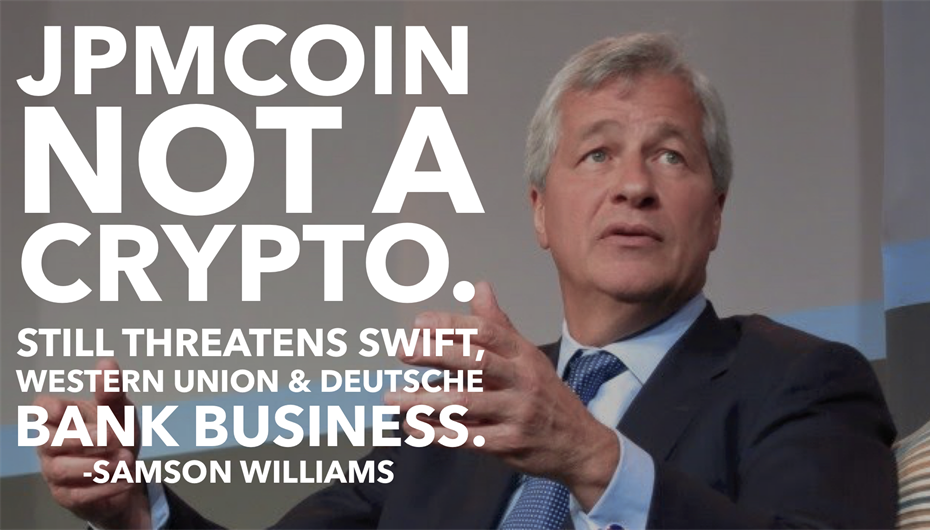

Last week JP Morgan announced that it had developed its own cryptocurrency, the“JPMCoin”. Lost in the much of the noise about whether or not the JPMCoin is a real blockchain or cryptocurrency is the fact that, for mainstream blockchain adoption, the announcement is a big deal. Don’t get me wrong. The JPMCoin is no more a cryptocurrency than say Fortnight’s V-Bucks or your airline miles are. However, for blockchain the technology (even if JPMorgan isn’t actually using a blockchain) the mere mention of the possibility that blockchain like tech is being adopted by the 6th largest bank in the world, a meaningful way, is a big step towards mainstream adoption.

As you consider this here are a few points you can confidently share with your colleagues and friends:

- The #JPMCoin isn’t a #blockchain or a #cryptocurrency

- That doesn’t matter because JPMorgan’s modern day #DigitalAbacus does solve real business problems and proposes real operational cost savings, aka revenue generators

- #Swift, #WesternUnion & #DeutsheBank should be concerned because when the worlds 6th largest bank adopts a means of saving X% on #settlement, #creditcard, #remittance and #banktransfers this could directly cut into their core revenue streams

- Because JPMorgan didn’t adopt #blockchainlike technology for accounting, for the greater good of transparency, trust, blah blah blah

- They did it for operational efficiencies that would translate into revenue 6 Coincidentally, Ripple rejoices! As the #JPMCoin validates their entire business model as only the 6th largest bank in the world can.

Too, JPM’s entry into the internal/private permissioned psuedo #blockchainworld of operational efficiency disrupts Ripple’s competitors. This is a blessing for Ripple, as it is easier to take down a global banking middlemen (Swift) if another global banking titan (JPMorgan) decides it wants to cannibalize its fellow banking middleman.

In conclusion, if you look beyond the hype you’ll see a landscape of operations & technology innovations, with incremental process improvements that = real $$$$. Too, you’ll see an international chess board where the major players are strategically positioning their businesses to take advantage of the most efficient (profitable) and complementary services available. Stay tuned. Blockchain in finance and banking is just getting started. Next, regulatory hurdles.

About the Author

My name is Samson Williams. I am a Professor at the University of New Hampshire School of Law, human and an anthropologist at Axes and Eggs. You can follow me on Twitter or Instagram @HustleFundBaby and on LinkedIn. And i encourage you to share this post and feel free to tag me in relevant post. Finally, I would say thoughts are my own but I probably stole them from a woman. #mansplaining #equalpay

Register for FREE to comment or continue reading this article. Already registered? Login here.

0